How digital-led insurance brands turn more leads into policies with full-funnel optimization, better tracking, and lifecycle journeys

If you’re a digital-led insurance brand in Nigeria or across Africa, this scenario probably sounds familiar: your lead numbers look impressive in Monday morning reports, but when your CFO asks about actual policies written, the numbers tell a different story.

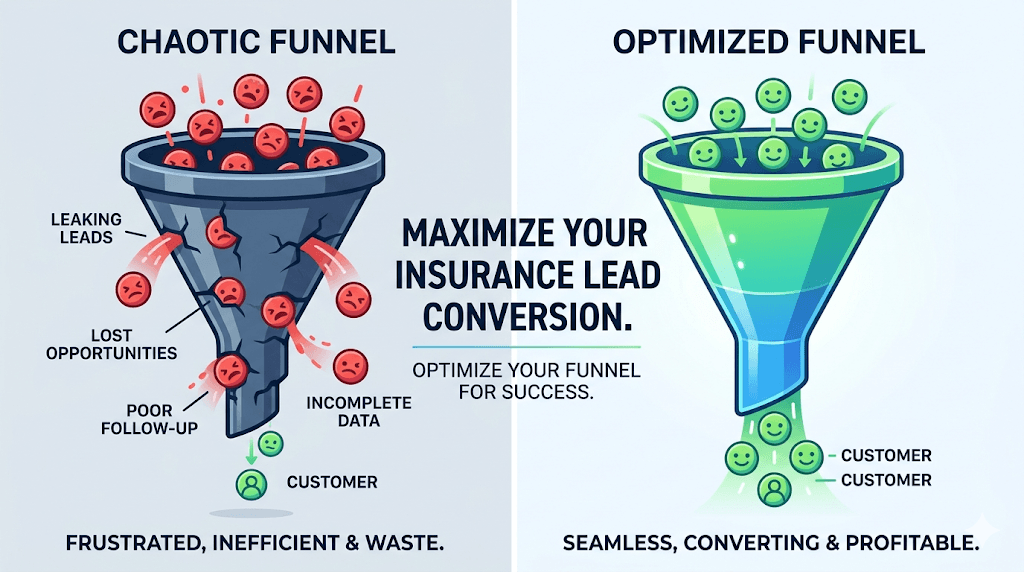

You’re not alone. Most insurance brands are losing 60-80% of their leads somewhere between “Get a Quote” and “Policy Issued” – and they don’t know exactly where or why.

The problem isn’t that you need more leads. The problem is that most insurance marketers are still thinking in channels and campaigns, not customer journeys.

Why Your Lead Numbers Look Great But Your Policies Don’t

At Intense Digital, we work with digital-first insurance brands across Africa and the UK, and we see the same pattern repeatedly: marketing teams are measured on leads generated, so they optimize for leads. Performance is tracked in clicks, impressions, and form fills – all the metrics that make dashboards look healthy but don’t pay the bills.

Meanwhile, three critical problems are killing your conversion:

1. The Quote-to-Policy Gap is a Black Box

Between someone requesting a quote and actually purchasing a policy, there are multiple steps: quote delivery, quote review, objection handling, payment, and policy activation. Most brands can’t tell you which step is losing the most customers or why.

2. Your Data Doesn’t Connect

Leads come through your website. Some go to agents. Others flow into your app. Payment happens through a third-party gateway. Your marketing team sees one set of numbers in Google Analytics, your sales team has different numbers in the CRM, and your finance team is working from yet another source.

When data doesn’t connect, you can’t make decisions – you can only make guesses.

3. Onboarding and Activation are Afterthoughts

Most insurance brands invest heavily in acquisition (ads, lead generation, brand campaigns) but treat onboarding as a “operations problem.” The welcome email is generic. Follow-up is manual or non-existent. There’s no systematic nurture for people who requested a quote but didn’t buy.

The result? You’re pouring water into a leaky bucket.

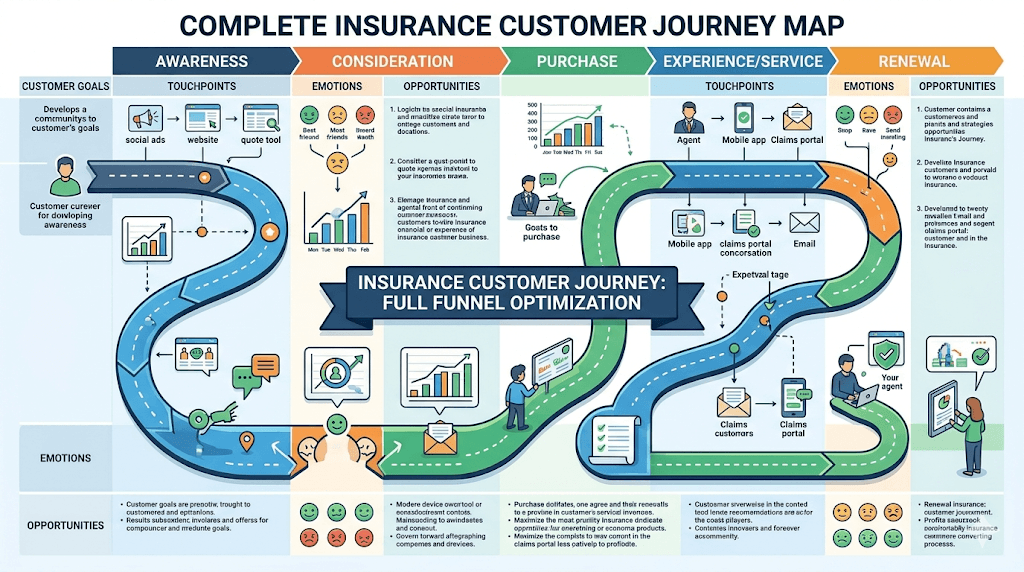

The Full-Funnel Approach: From First Impression to Policy Renewal

Growth marketing for insurance isn’t about running more ads. It’s about designing and optimizing the entire journey – from the first impression to the first policy, and from first policy to renewal and referral.

Here’s how we reframe the work:

Stage 1: Acquisition with CAC and Payback Discipline

Yes, you still need leads – but the right leads, acquired at the right cost, with clear payback visibility.

Instead of celebrating a “successful campaign” because it generated 1,000 leads, we ask:

- What’s the cost per quote request?

- What’s the quote-to-policy conversion rate?

- What’s the effective CAC (cost to acquire an actual policyholder)?

- What’s the payback period on that CAC, given your premium and renewal rate?

Action: Before you scale any campaign, map the full cost from click to policy, and set a maximum acceptable CAC based on your LTV.

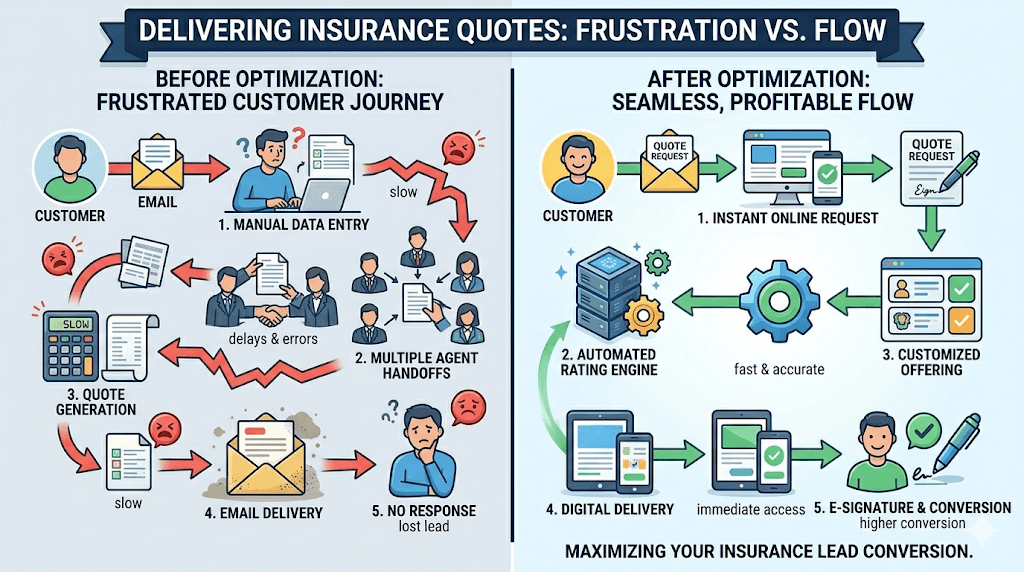

Stage 2: Activation – Turning Quote Requests into Policies

This is where most insurance brands lose the game.

Someone requests a quote. What happens next? Do they get the quote instantly, or does it take 24-48 hours? Is it delivered via email, SMS, WhatsApp, or agent call? Is the quote clear and simple, or does it require a manual phone call to understand?

Every point of friction is a point of drop-off.

What we optimize:

- Speed: Instant or near-instant quote delivery wherever possible

- Clarity: Quotes that are easy to understand without requiring a phone call

- Nudges: Automated follow-up via email, SMS, or WhatsApp if the quote isn’t accepted within 24-48 hours

- Objection handling: Proactive messaging that addresses common questions (e.g., “Is this really comprehensive?” “What happens if I need to claim?”)

Real example (anonymized): For a motor insurance client, we rebuilt the quote delivery flow and added a simple 3-message WhatsApp sequence for non-converters. Quote-to-policy conversion lifted by 34% in 60 days, with zero increase in ad spend.

Stage 3: Retention and Renewal Journeys

Acquiring a policyholder is expensive. Renewing them is far cheaper – and often more profitable.

Yet most insurance brands treat renewals as an administrative task, not a marketing opportunity. Renewal reminders go out 7 days before expiry, often via a generic email that half the customers don’t see.

What a good renewal journey looks like:

- 60 days before expiry: “Your renewal is coming up – here’s what’s covered”

- 30 days out: “Renew early and save X%” or testimonial/claims story to reinforce value

- 14 days out: Direct nudge via SMS and email

- 7 days out: Final reminder with one-click renewal link

- Post-renewal: Thank-you message + referral prompt (“Know someone who needs cover?”)

Retention rate improvements of even 5-10% have an enormous impact on LTV and the unit economics of your entire acquisition engine.

Stage 4: Referral and Advocacy

Happy policyholders – especially those who’ve had a good claims experience – are your best acquisition channel.

Yet most brands never ask for referrals, or they ask once in a generic email that gets ignored.

Simple referral tactics that work:

- Post-claim follow-up: “Glad we could help – know anyone else who needs cover?”

- Renewal thank-you message: “Thanks for renewing – refer a friend and you both save”

- Incentivized referral program tracked via unique links

Referrals typically have higher conversion rates and lower CAC than cold acquisition, and they compound over time.

Fixing the Foundation: Tracking, Data and Marketing Ops

None of the above works if you can’t measure it.

The unglamorous truth is that many insurance brands are flying blind. Broken tracking, duplicated events, missing conversion tags, and disconnected systems mean the data you’re using to make decisions is incomplete or wrong.

The 5 tracking issues we see in almost every new insurance client:

- Form submissions tracked, but not actual policy issuance – so you can’t measure true conversion

- No conversion value tracking – you know someone bought, but not the premium value

- Multi-step funnels not instrumented – you can’t see where drop-off happens

- Agent-assisted conversions not attributed – offline and online aren’t stitched together

- Multiple sources of truth – marketing, sales, finance, and operations all use different numbers

Before we scale anything, we fix this. We implement clean event tracking (usually via GA4 and server-side tagging where needed), build a single source of truth dashboard, and make sure every decision-maker is looking at the same numbers.

Action: Audit your tracking this month. Can you answer these questions with confidence?

- What’s our true cost per policy (not cost per lead)?

- Where in the journey are we losing the most people?

- What’s our payback period on acquisition spend?

- What’s our renewal rate by cohort?

If the answer is no, fix your data before you spend another dollar on ads.

The Growth Scorecard Your CFO Will Actually Respect

Forget the campaign report full of impressions, reach, and engagement. Here’s what your CFO and EXCO care about:

| Metric | Definition | Why It Matters |

| CAC | Total acquisition cost ÷ policies issued | Are we spending efficiently? |

| Payback Period | How many months to recover CAC from premiums | Can we afford to scale? |

| Quote-to-Policy % | Policies ÷ quote requests | Are we converting interest into revenue? |

| Renewal Rate | % of policies renewed at expiry | Are we keeping customers? |

| LTV | Average premium × retention period | What’s a customer worth over time? |

| LTV:CAC Ratio | LTV ÷ CAC | Is this a good investment? |

At Intense Digital, we build this scorecard with every insurance client in the first 30 days, and we review it monthly with the leadership team. It changes the conversation from “how many clicks did we get?” to “are we growing profitably?”

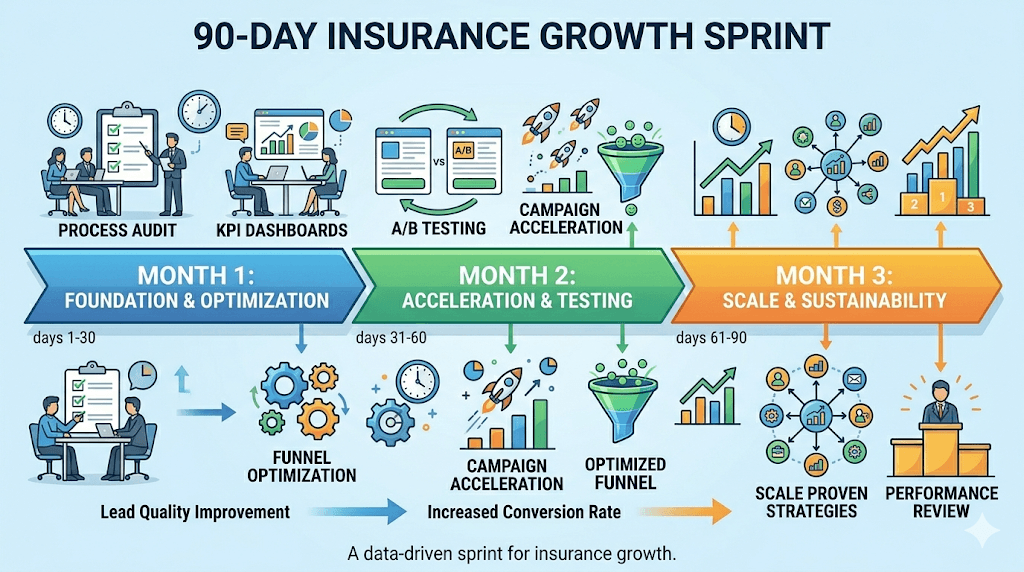

90-Day Growth Sprint: What We’d Do First

If we were stepping in as your growth partner today, here’s what the first 90 days would look like:

Weeks 1-4: Diagnose and Fix Foundations

- Audit the full funnel from ad click to policy issuance

- Map where leads are dropping off

- Fix tracking and build the growth scorecard

- Identify the top 3 highest-impact opportunities

Weeks 5-8: Activation and Conversion Experiments

- Optimize quote delivery speed and clarity

- Implement abandoned quote follow-up sequences (email, SMS, WhatsApp)

- A/B test landing pages and form flows

- Improve payment experience (reduce steps, add payment options)

Weeks 9-12: Retention and Scale

- Build or optimize renewal journey

- Implement post-purchase onboarding and engagement flows

- Launch simple referral program

- Scale acquisition on channels and campaigns with proven payback

Each sprint is built around a backlog of prioritized experiments – small tests that compound into meaningful revenue gains.

From Campaigns to Growth Systems

Most insurance brands are still playing the old marketing game: run a campaign, generate some leads, hope some of them convert, then run another campaign.

The new game is about systems – building a repeatable, measurable, optimizable engine that turns investment into predictable revenue.

It’s not sexier. It’s not built around one big idea or creative concept. But it works, and it scales.

At Intense Digital, we help digital-first insurance brands build that engine. We design and optimize the full journey, we measure what your CFO cares about, we run continuous experiments, and we fix your data so growth decisions aren’t guesswork.

We don’t want to be “the agency over there.” We plug into your team, co-own targets with your leadership, and work off a shared dashboard so everyone can see what’s working, what’s not, and what we’re testing next.

Ready to turn more leads into policies?

We offer a complimentary 30-minute funnel teardown where we’ll walk through your current journey, show you where we see the biggest opportunities, and outline what a 90-day growth sprint would look like for your brand.